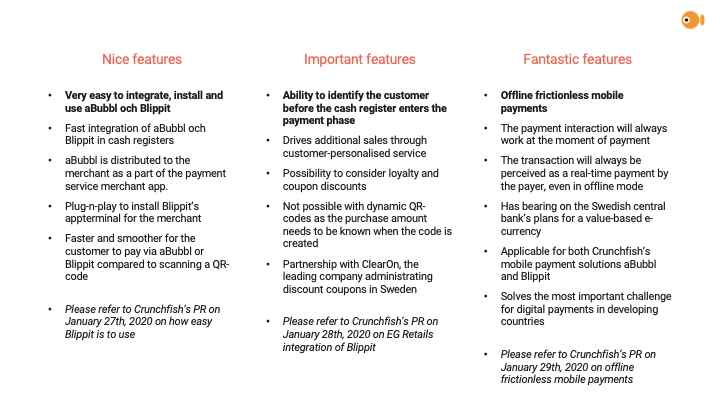

Crunchfish enables offline frictionless mobile payments

This is a huge breakthrough and has strong potential to change the global payment eco-system and accelerate the transition from card payments to real-time payment systems. This patent pending innovation makes modern digital payment services far more robust, as the moment of payment functions in the same way, regardless of whether the payer and/or the […]

This is a huge breakthrough and has strong potential to change the global payment eco-system and accelerate the transition from card payments to real-time payment systems. This patent pending innovation makes modern digital payment services far more robust, as the moment of payment functions in the same way, regardless of whether the payer and/or the payee is offline.

Digital payments are potentially unreliable. We have all experienced not being able to complete a transaction. This can be due to poor internet access, no mobile coverage or that the whole payment service is down. In countries with less developed IT-infrastructure this is an even greater issue and probably the greatest obstacle standing in the way of full digitalisation of payments.

Crunchfish tackles this problem by offering offline frictionless mobile payments. The transaction works even if neither the payer or payee have access to the internet, don’t have mobile network coverage or aren’t connected to the payment service backend. We make this possible by differentiating between the moment of payment and the transfer of money in the cloud. In order to have funds to use offline the user can either: reserve money in their bank account for offline use, arrange credit for offline payments or preferably make a digital withdrawal from their bank account to their mobile app. This is the digital equivalent of taking out money at an ATM and carrying the cash around in your wallet. The digital money is placed in a mobile wallet and can be used in the same way as cash. This innovation has the potential to support the Swedish Central Bank’s plans for a value based e-currency.

The offline payment works just as well for aBubbl, where the mobile transaction is done straight to an app on the payee’s mobile or tablet, as it does for Blippit, where the mobile transaction goes via Blippit’s app terminal to a physical cash register in store.

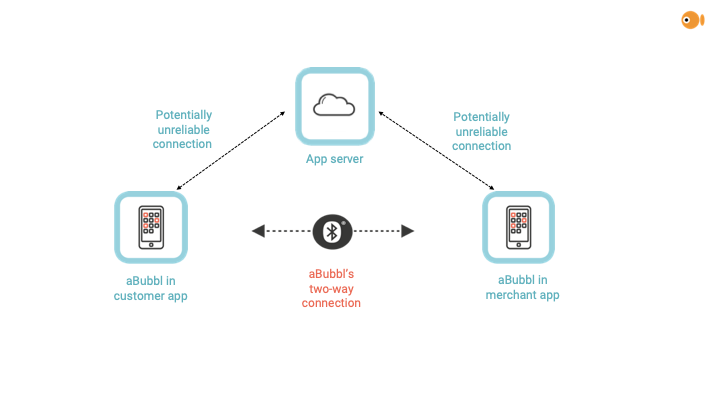

Figure 1: aBubbls architecture where Crunchfish’s only counterpart is the digital payment service. This makes very fast roll-out for aBubbl possible.

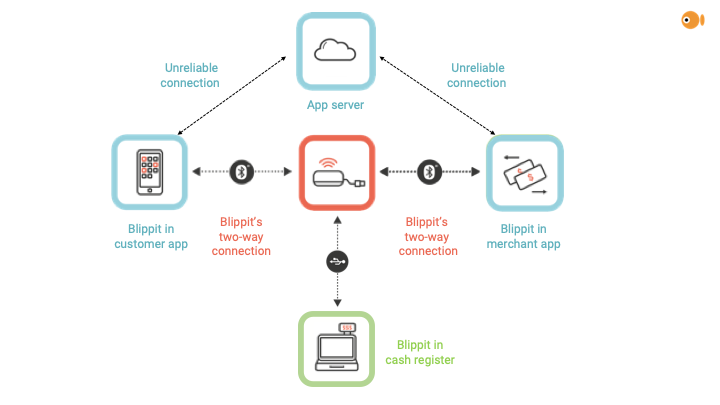

Figure 2: Blippit’s architecture where Blippit is integrated into the digital payment service and also by the cash register supplier. This makes the app terminal plug-n-play for the merchant.

At the moment of payment the transaction is digitally signed by the payer and transmitted locally to the payee, so the payee has a digitally signed commitment, similar to a guaranteed check. If both parties are offline at the moment of payment, the transfer of money will take place later when one of the parties has internet connection and access to the payment service’s back-end in the cloud. All the transactions are logged locally by both the payer and the payee and updates the offline digital balance of both parties. In those cases where one or both parties are online, the transfer of money takes place at the moment of payment.

With real-time payments, the most common way to inform the payer about who will receive payment, is for the payer to scan a QR-code that contains the payee details. It is possible to include the QR-code amount with a so called dynamic QR-code that always has to be shown on a digital screen. If you have been to China or India you quickly learn to scan QR-codes at payment, as this method is used everywhere. With QR-codes the communication is always one-way towards the unit scanning the QR-code. The QR-code is simply an image and cannot receive any information. This is in contrast to the local two-way communication that both Crunchfish’s Bluetooth based mobile payment solutions are based on.

This creates huge advantages and enormous possibilities for Crunchfish, especially for markets where internet connection and sometimes even mobile coverage is a problem. The two largest markets in the world for real time payments, China and India, experience these problems but the problem exists everywhere, even in countries with relatively good connectivity. Since QR-codes only make one-way local communication possible, internet connection and communication via the payment service in the cloud is needed for both the payer and receiver in order for them to digitally register the payment. Crunchfish’s breakthrough complements the ecosystem for QR-codes since payments will be able to be made, even if one or both of the parties are offline. This will still be perceived as a real-time payment.

For more information contact:

Joachim Samuelsson, CEO Blippit

+46 708 464 788

joachim.samuelsson@crunchfish.com

Joakim Nydemark, CEO Crunchfish

+46 706 35 16 09

ir@crunchfish.com

About Crunchfish – crunchfish.com

Crunchfish AB (“Crunchfish”) develops and markets patented interaction solutions for mobile payment and augmented reality. The business regarding mobile payment takes place in the subsidiary Crunchfish Proximity with a focus on proximity-based interaction. With an inhouse developed app terminal and related software, Crunchfish makes ‘blipable’ coupons and payments possible. The commercialisation is done together with ClearOn in the jointly owned company Blippit. Within AR, the company offers software that enables gesture control in AR glasses and other consumer electronics. The software is one of the leading in the world and exists in tens of millions of units on the market through clients like OPPO, Vuzix and Lenovo. Crunchfish is listed on Nasdaq First North Growth Market since 2016. The company was founded 2010 with head office in Malmö, Sweden.