A Deep Fintech Company

Crunchfish provides a patented layer-2 offline payment solution designed for payment network providers as well as payment service providers. The company’s Digital Cash solution enables survivability in the face of failure in case of fluctuating internet connections and system failures by striking the perfect balance between security and scalability whilst integrating offline payments in an online world.

Crunchfish Digital Cash Timeline

Patented Leadership

Crunchfish leads the innovation race for offline payments with online settlement.

Protected areas

Offline payments

Trusted Client Applications

Proximity interaction

Priorities from 2018.

16

UNIQUE INNOVATIONS

6

GRANTED INNOVATIONS*

*Includes positive International Preliminary Reports on Patentability (IPRP)

Survivability in the Face of Failure:

Offline payments ensure economic resiliency by enabling transactions to occur even in environments with no or unreliable internet or service connectivity. From rural merchants in remote areas to urban customers impacted by network or service disruptions, the ability to perform offline transactions is rapidly becoming an essential feature of modern financial ecosystems.

Despite their growing importance, current offline payment systems face several challenges:

Double spending is an inevitable security risk of offline payments.

Particularly evident in solutions requiring hardware-based secure elements for wallets and terminals, as no efficient ecosystem exists for large-scale application deployment and upgrades.

The widespread reliance on Fund, Pay, Defund, and Reconcile (FPDR) models introduces adjunct layers that require separate reconciliation frameworks, complicating adoption.

Recognizing these limitations, Crunchfish has engineered a modular offline payment system combining interoperability, security, and scalability into a streamlined architecture that may be integrated with any type of underlying payment scheme.

In the paper “The design philosophy of the DARPA Internet Protocols” published in 1988 by David D. Clark from Massachusetts Institute of Technology outlines that the internet fundamentally is “a packet switched communication facility in which a number of distinguishable networks are connected together using packet communications processors called gateways which implement a store and forwarding algorithm”.

Crunchfish Digital Cash is inspired by the design philosophies that was developed by the Defense Advanced Research Projects Agency (DARPA) in the 1970s and became the internet as we know it today. It is an incredible robust protocol based on packet switching. This is how Crunchfish Digital Cash works for payments. He also outlines seven secondary design goals for TCP/IP, for which Crunchfish Digital Cash has an equivalent and patent-pending Trusted Application Protocol (TAP). Crunchfish Digital Cash is based on the same design principles and may deliver for digital payments what the internet has done for digital communications.

Any public good in the society like the internet, electricity or telecom must be carefully designed to continue working despite temporary outages of the service. It is hard to understand why digital payments, certainly also a public good, is not as robust as other public goods. Digital payments service must be as robust, inclusive and private as cash payment.

Interoperable Offline Wallets

Offline wallets are the payer component, allowing users to initiate and sign offline transactions securely. In peer-to-peer payment scenarios, offline wallets acts also as receiving components, enabling consecutive offline payments. Crunchfish Digital Cash Offline Wallet is a secure and scalable component that executes within a Virtual Secure Element providing an isolated runtime execution environment.

Crunchfish Digital Cash Offline Wallets supports various other proximity interaction methods (NFC, Bluetooth, Ultrasound), catering to different use cases and ensuring broad compatibility. The QR-based interaction method is highlighted below for its effectiveness in accommodating low-end devices and as a reliable backup system.

Wallet-to-Wallet:

The payer displays a QR code representing their offline wallet transaction, which the payee scans to complete the payment.

Wallet-to-Terminal:

A merchant or payee presents a QR code with a payment request, which is scanned by the payer. The payer generates the offline transaction and displays a QR code representing their offline wallet transaction, which the payee scans to complete the payment.

Offline Payment Demos

Proximity Offline Payments

Using QR

Using QR and Bluetooth

Using QR and ultrasound

Using NFC and Bluetooth

Consecutive offline payment

Using QR and Face ID

Remote Offline Payments

Using telecom

Offline Wallets in Secure Elements

Whether using a software-based virtual secure element, a trusted execution environment (TEE) or an embedded secure chip, offline wallets must at least guarantee isolated runtimes and encrypted storage for sensitive data at rest.

However, operational challenges are present for large-scale deployment of hardware-based solutions, including monitoring, upgrades, and compliance.

Offline Wallet Communication

The architecture enables offline wallets, offline terminals, and the backend servers to communicate in a standardized way across multiple proximity and remote APIs, including:

- Proximity Mechanisms: NFC, QR, Bluetooth or ultra-sound for offline interactions.

- Remote APIs: Wallet and backend communication when partial connectivity is available.

The PKI framework ensures data end to end security across all communication channels, enforcing the same standards

The alignment of offline wallets with the operational capabilities of standard e-wallets presents a transformative approach to initiating payments. By leveraging security, convenience, and accessibility, offline wallets can provide essential functionalities for users, mirroring the reliability of online payment methods.

In a world where connectivity is not always guaranteed, offline wallets stand to bridge the gap, enabling users to engage in digital transactions smoothly, irrespective of their location or connectivity status. This evolution not only broadens the reach of digital payments but also fortifies financial inclusion on a global scale.

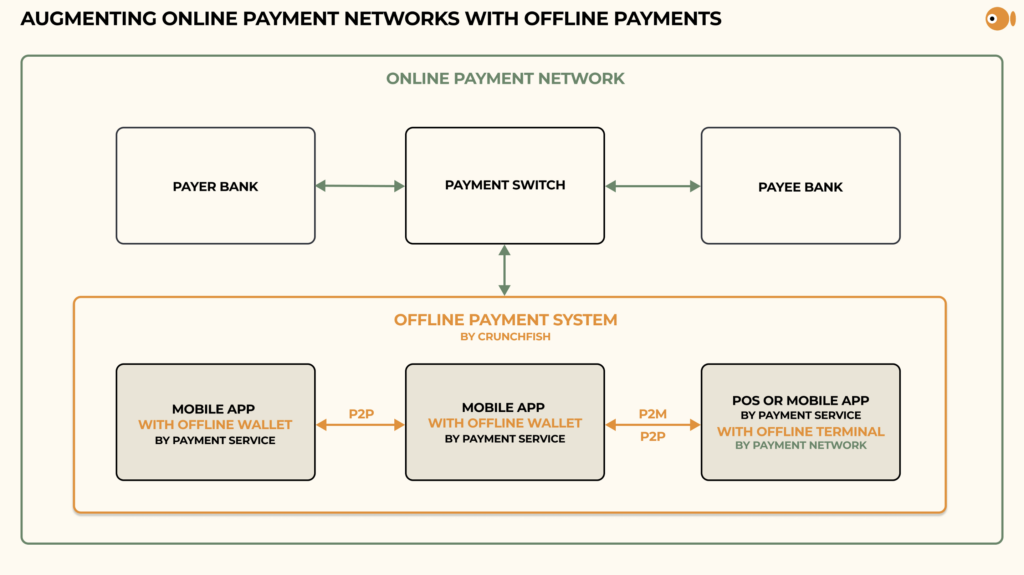

Offline Terminal Infrastructure

Offline terminals are the receiving component, an integral part of the payment rail infrastructure provided by the payment networks. They act as universal receivers of offline payments, ensuring that merchants, payees, and the backend across the ecosystem, can seamlessly verify and accept offline transactions regardless of the type of offline wallet used by the payer.

Form factors:

are suitable for light-weight integrations (e.g., mobile app-based solutions) for merchants or person-to-person payments.

are dedicated physical POS devices for larger merchants or institutions performing high volumes of offline transactions.

can either be the payment network providers, payment service providers, or payment application providers, as long as they comply with standardized specifications.

Like EMVCo systems, the modular design separates terminals and wallets, ensuring interoperability and standardization.

- – EMV Terminal Infrastructure: In EMVCo systems, acquiring terminals ensure that payments can be received universally across the ecosystem. Similarly, the Offline Terminal Infrastructure serves as the foundational component for receiving payments, validating payer-side interactions securely and reliably.

- – Card Issuance Model: EMVCo chips or cards from financial providers function as standardized payment origination tools. Similarly, Offline Wallets are the tools for initiating offline payments, provided as secure, standardized solutions aligned to payment network specifications.

- – Standardization and Interoperability: EMVCo’s specification enables issuers, acquirers, and merchants to operate on common standards. Similarly, this modular offline system ensures that terminals and wallets stay interoperable regardless of provider or user preference.

The benefits are a clear modular separation between receiving and paying components reduces implementation complexity and standardized specifications (e.g., for offline terminals and offline wallets) that foster competition and innovation within the ecosystem.

Offline Payments in an Online World

The Reserve, Pay, and Settle approach optimizes offline payments by leveraging existing rails for online settlement rather than relying on separate reconciliation layers. The modularity of this unique approach of offline payments combines the interoperability of EMVCo card payments with the programmable flexibility of Ethereum smart contracts, delivering a comprehensive framework for secure offline transactions.

The Reserve, Pay, and Settle approach optimizes offline payments by leveraging existing rails rather than relying on separate reconciliation layers:

Pre-authorizing funds ensures trust without immediate backend connectivity.

Enable secure offline transactions validated by terminals.

Offline transactions are reconciled through online settlement structures, preventing fraud and enhancing efficiency.

The proposed Reserve, Pay, and Settle approach for offline payments aligns closely with Ethereum’s smart contract-based systems, emphasizing programmable constraints, secure execution, and standardized interactions.

- – Programmable Constraints for Settlement: In Ethereum’s smart contracts, payments or transactions are executed based on pre-defined conditions programmed within the contract. Similarly, Reserve, Pay, and Settle (RPS) introduces settlement constraints for offline payments, ensuring funds are reserved before they are paid and reconciled securely once connectivity is restored. This parallels the way smart contracts enforce trust between parties without requiring a central intermediary for real-time validation. Offline payments achieve this trust by securely signing transactions in the wallet using cryptographic methods (such as PKI).

- – Deterministic Execution in Isolated Environments: Ethereum’s smart contracts execute within the Ethereum Virtual Machine (EVM), providing a tamper-proof environment for deterministic processing. Similarly, offline wallets in secure elements, whether virtual software-based or hardware-based, provide isolated runtimes to ensure the integrity of transaction signing and execution. For both approaches, isolated execution environments prevent external tampering and ensure transactions are initiated securely.

- – Automation and Reconciliation: Smart contracts on Ethereum automate the settlement of transactions once predefined conditions are met, such as event triggers or external approvals. Similarly, the Reserve, Pay, and Settle approach automates the reconciliation process, validating offline transactions during online settlement and ensuring any conditions related to the payments — such as constraints on spending limits or usage validation —are enforced securely.

The benefits of this Reserve, Pay, and Settle approach is a trusted framework where offline payments rely on cryptographic trust mechanisms, just like Ethereum’s smart contracts, to ensure integrity during execution, mitigating risks such as double spending. The Ethereum smart contracts operate universally on the blockchain via standardized protocols. Both approaches prioritize transaction security, leveraging isolated execution environments and cryptographic validation to maintain transactional integrity. Conditional offline payments introduce advanced use cases similar to programmable systems on Ethereum, such as escrow, pay-per-use models, or government-disbursed subsidies with strict conditional rules for usage.

Contact us to learn more